An Introduction to Instant Payments for Business Credit Executives

By David Schmidt

Now that FedNow has launched, US-based sellers should anticipate greater access to instant payments. Europe has enjoyed access to instant payments since the Bank of England launched Faster Payments in 2008, which has been widely accepted and continues to grow. Since then, a host of other countries in Europe, Asia, and South America have also launched similar 24/7 payment platforms. Instant payments gained traction in the US in 2017 with the launch of RTP (Real-Time Payments) by The Clearing House, a consortium of leading banks, but not everyone in the US has enjoyed access to this facility.

While paper checks still exist, the future of money, particularly for larger enterprises, lies in instant payments. FedNow represents a significant upgrade to the United States’ payment technology, offering a more convenient and efficient way to move money compared to current options, and often at a fraction of the cost.

Business leaders need to prepare for this change by adjusting their mindsets. The traditional notion of money movement during working hours will be replaced by round-the-clock accessibility, as FedNow allows payments to be deducted from accounts 24/7. This shift requires adopting continuous accounting practices that update books in real-time as money moves. Payment infrastructures also need to be revamped to take full advantage of FedNow, replacing batch processes with real-time workflows. Additionally, fraud checks must be strengthened due to the irrevocable nature of real-time payments.

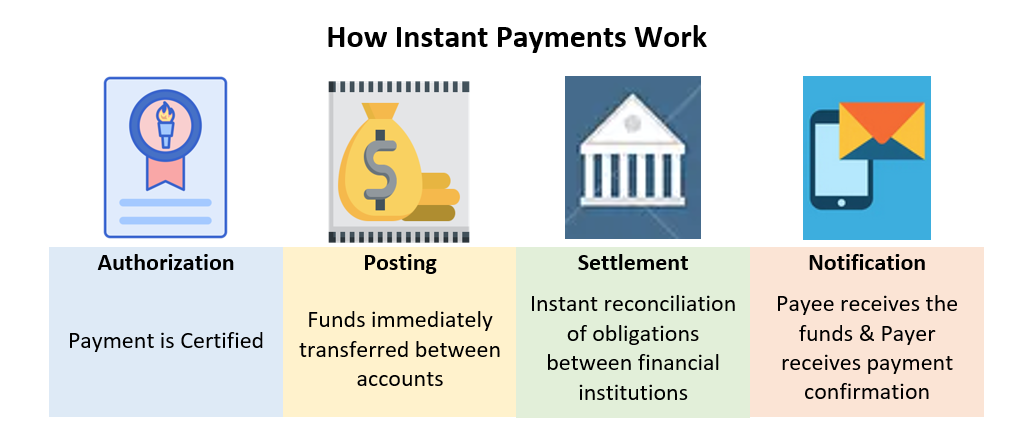

The current primary method of electronic money transfers in the US, the Automated Clearing House (ACH), is outdated and limited in its availability, often taking one to three days to complete transactions. At the same time, RTP adoption has been hindered by high costs, charging 25 cents to $1 per payment, and limited participation from banks.

FedNow addresses these challenges by offering a more cost-effective solution for banks. FedNow will operate 24/7 and allow businesses that accept commercial credit cards or other forms of payment in advance to instead initiate requests for payment. The customer can simply approve the payment eliminating the need for getting credit card numbers, with greatly reduced transaction fees, and no chargeback risks. The convenience of FedNow rivals that of wire transfers but at a significantly lower cost and no end-of-the-day window.

Smaller businesses, especially those struggling with cash flow, may find some relief thanks to instant payments and FedNow serving an alternative to credit cards with their high fees. Surveys suggest that roughly half of US small businesses struggle financially, so this impact could be substantial.

The changes brought about by FedNow present opportunities for streamlined payments and innovation, making it crucial for all businesses to prepare for this upcoming shift. Besides accelerating cash flow, instant payments should prove to be a critical component of more secure supply chains.

The Key Differences Between FedNow and the RTP Network

FedNow and the RTP network are the two systems in the United States that facilitate real-time clearing and settling of payments, but they have some key differences. While both systems aim to achieve the same outcome of real-time payment processing, their operational structure, accessibility, and transaction limits differentiate them from each other.

FedNow is operated by the Federal Reserve as a federal system, while RTP is a privately run system owned and operated by The Clearing House, a consortium of banks. This distinction makes FedNow more accessible to banks of all sizes across the country.

Another difference lies in transaction limits. FedNow has a maximum transaction limit of $500,000, while RTP allows transactions up to $1 million. This means that for larger payments, banks will still need to rely on the Fedwire system.

RTP currently reaches about 65 percent of US bank accounts and has nearly 300 banking participants across the country out of a pool of over 8,000 banks and credit unions. Since only a small percentage of banks use the RTP network for both sending and receiving payments, there is still much progress to be made in terms of adoption.

Several banks, including BNY Mellon, Citi, Citizens Bank, JP Morgan Chase, and Wells Fargo, participated in the pilot or are adopting FedNow. Some of these banks see FedNow as a complementary addition to their existing instant payment offerings. Companies offering trade credit need to explore the adoption of FedNow with their financial institutions, as well as any payment platform providers with whom they already have a relationship, to better understand these financial partners’ FedNow adoption plans. That’s the first step toward implementing instant payment capabilities, whether your company is extending credit or relying on other payment channels to meet your customers’ needs.

Editors Note: Here are some recent postings in Credit Today about FedNow and Instant Payments:

- Request-for-Payment Technology Promises to Accelerate Collections

- Federal Reserve Names Organizations Certified as Ready for FedNow Service

- The Federal Reserve Announces July Launch of the FedNow Service

- Federal Reserve Announces Intent to Create a Real-Time Payments Network

- World’s Major Economies Playing Catch-Up as Widespread Adoption Drives Global Real-Time Payments Growth – ACI Worldwide Report

- ACI Worldwide Creates Faster Pathways to U.S. Real-Time Payments Systems with Integrated Fraud Safeguards