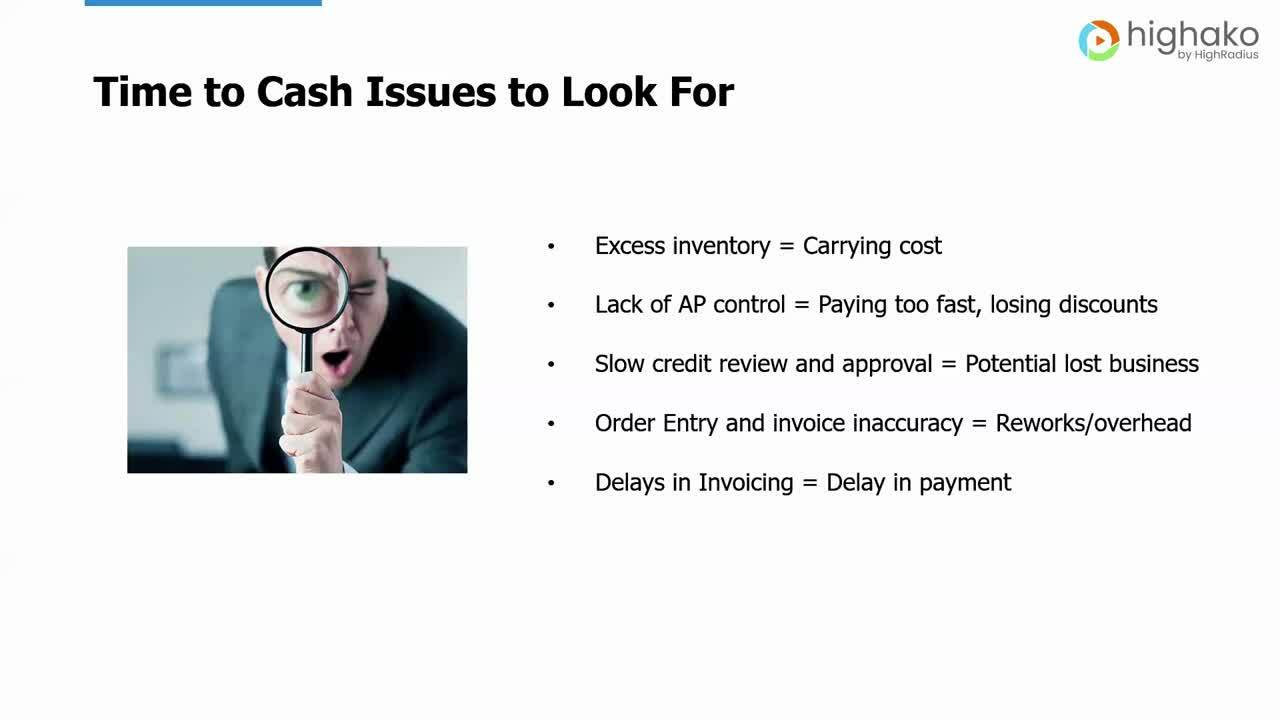

Working Capital Efficiency: The Key to Understanding Your Customer's Cash Flow

With liquidity being the primary driver of your customer's ability to pay you in a timely manner, what should analysts be looking for? What are the keys to this? The answer lies in Working Capital and this article gives a practical tutorial on what to look for.

Let's start at the beginning: You probably know that Working Capital represents the difference between current assets and current liabilities. Historically, analysts, in a quick review, looked at the Current Ratio (current assets divided by current liabilities) as a representation of the relationship. This indicator has well-known limitations (see "Current Ratio: A Good Indicator or a False Signal?"), one of which is the condition of the current assets such as inventory and receivables. You'll need to dig a little deeper, looking more closely at some of these individual components. And look at the "operating cycle," where inventory is acquired, turned into accounts receivable as a result of the sale, and when collected, turned into cash, which is used to pay trade creditors, among others.

To get a feel for the quality of inventory, you should look at how quickly it turns over (measured in days with the metric "Days Inventory Outstanding"). Looked at another way, this is the speed with which inventory is converted into a receivable.

Just like inventory, the quality of A/R is largely measured by how fast it turns, and this is a function of their terms and the quality of the customer base (including your customers' ability to collect it!). Once again, knowing the industry, you should have a feel for good, mediocre, or poor Days' Sales Outstanding numbers.

Days Payable Outstanding's Place in the Operating Cycle

The operating cycle, which starts with inventory turning into A/R, and then back to cash, also includes how long the company takes to pay its suppliers for its inventory. So it changes depending upon how long a company takes to pay its suppliers, with Days Payable Outstanding ("DPO"), or the average length of time it takes to pay suppliers, as the metric for this.

Knowing the industry, you can estimate a quick, average, or slow turn of inventory. Faster is of course always better; without successful inventory management routines, it takes longer to turn into accounts receivable.

Understanding the operating cycle is important when analyzing a business because it's a good measure of overall efficiency. The faster a company can turn its investment in inventory and receivables, the more quickly it generates cash. This gives it more flexibility and for the creditors of the company, less risk. And, if the business can get longer terms from its suppliers, it can accept slower turns in inventory and receivables without restricting cash flow.

For perspective on how CFOs think about these metrics, I was at a Construction Financial Management Association (CFMA) meeting recently and there was a panel discussing this. One member spoke about the cash conversion cycle and noted that when his receivables or inventory is slow, he has some flexibility by slowing down his payables (thus keeping his cash conversion cycle the same number of days).

So, to sum up: Days Inventory Outstanding (DIO) plus Days Sales Outstanding (DSO), fewer Days Payable Outstanding (DPO), gives you the Cash Conversion Cycle (CCC) in days.

A company always has an interest in reducing its cash conversion cycle because of carrying costs. Today's trend of customers asking for (or sometimes demanding) extended terms relates directly to improving their CCC by stretching suppliers' terms. And these four measures tell you how efficiently a customer is managing its operating cycle and working capital . . . which is supposed to be in motion and working.

So What's the Bottom Line?

So why does this matter to you as a Trade Creditor? If your customer's inventory or receivables slow down, the customer will generate less cash to meet obligations in a timely manner. And who gets paid last? If it takes longer to generate cash, the Trade Creditor -- always the weakest of the three primary parties -- is more at risk of not being paid in a timely manner.

The current ratio, the classic measure of liquidity, isn't much help to the Trade Creditor in projecting timely payment. Instead, DIO, DSO, DPO, and CCC, combined with knowledge of the customer's reserves and credit lines, are much more insightful.

Contact Information

Rod Wheeland, the former CEO of NACM Commercial Services, is President, of Wheeland Consulting

Phone: 503-705-7868

Email: rod@wheelandconsulting.com

LinkedIn.

|

Editor

|

.png)

|

|

|

|||||||||||